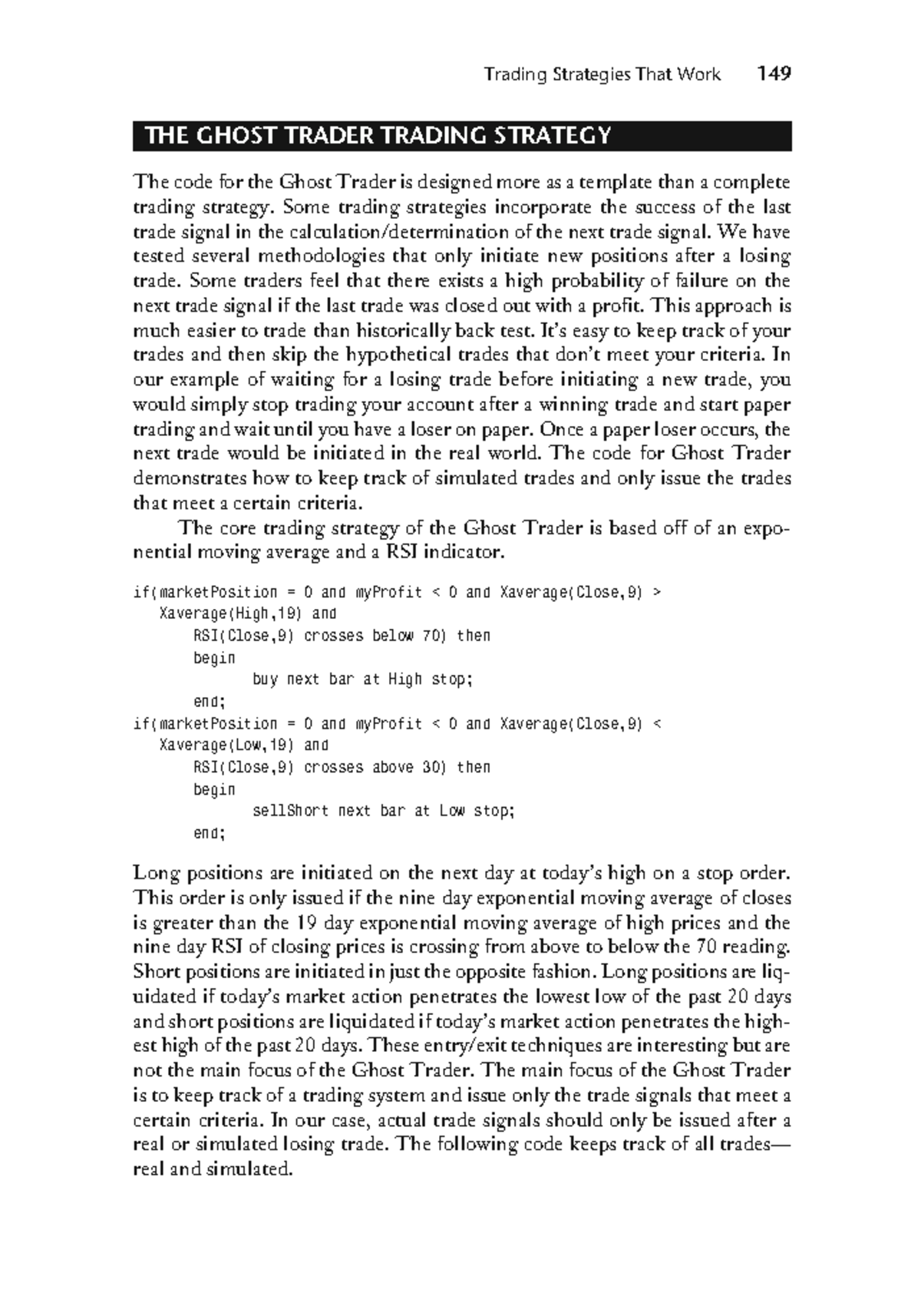

The United States has quietly extended a critical waiver allowing transactions with sanctioned Russian financial institutions for energy-related purposes, effectively signaling that keeping global gas prices low is a higher priority than tightening the noose around Moscow’s primary revenue stream. This move isn't a mere administrative hiccup. It is a calculated retreat. By pushing back the expiration of General License 8J, the Treasury Department is acknowledging a harsh reality that many in the West are hesitant to admit publicly: the global economy remains tethered to Russian crude, and any attempt to sever that connection too quickly risks a domestic political catastrophe.

The decision allows major international banks to continue processing payments for Russian oil and gas through entities like Sberbank, VTB, and the Central Bank of Russia. Without this extension, those transactions would have hit a legal wall, potentially freezing millions of barrels of oil out of the global supply chain overnight. For an administration facing an electorate sensitive to every cent of fluctuation at the pump, that was a risk not worth taking.

The Crude Reality of Supply and Demand

Sanctions are often sold to the public as a surgical tool designed to cripple an adversary’s economy while leaving the rest of the world unscathed. The truth is much messier. The global oil market is a tightly wound machine where the loss of even 1% or 2% of supply can send prices screaming upward. Russia remains one of the world's top three oil producers. If you remove their barrels, you create a vacuum that cannot be filled by Saudi Arabia or American shale producers on a moment's notice.

Washington’s "U-turn" is actually a return to pragmatism. The initial bravado of "total economic war" has met the cold, hard floor of market fundamentals. Energy experts have long warned that aggressive sanctions on Russian energy would act as a double-edged sword. While it drains the Kremlin’s war chest, it also acts as an inflationary tax on Western consumers. By extending these waivers, the U.S. is essentially choosing the lesser of two evils: allowing Russia to continue profiting from energy sales to ensure that the American middle class doesn't buckle under $5-a-gallon gasoline.

The Myth of the Price Cap

We were told the G7 price cap would be the ultimate solution. The idea was simple: allow Russian oil to flow, but only if it was sold below $60 per barrel. This was supposed to keep the market supplied while denying Putin the "excess" profits needed to fund his military.

It worked on paper. It failed on the high seas.

Russia responded by assembling a "shadow fleet" of aging tankers, operating outside of Western insurance and shipping circles. These vessels don't care about the G7 price cap. They operate in a gray zone, transferring oil ship-to-ship in the middle of the ocean and delivering it to refineries in India and China. Because these transactions happen outside the Western financial system, the price cap has become more of a suggestion than a rule.

When the U.S. extends these waivers, it is an admission that the shadow fleet has successfully bypassed the primary chokehold. If the West can't stop the oil from moving, the only thing it can do is ensure that the legal channels remain open enough to prevent a total market panic.

The Geopolitical Balancing Act

Every time a waiver is extended, it sends a message to allies and adversaries alike. To the Kremlin, it signals that the West's "red lines" are actually made of rubber. They can be stretched and moved based on the political needs of the sanctioning body. To allies in Europe who have made massive sacrifices to decouple from Russian gas, it feels like a betrayal of the collective mission.

However, the view from the Treasury Department is purely mathematical. They are looking at "spare capacity"—the amount of extra oil the world can produce if something goes wrong. Right now, that cushion is uncomfortably thin.

- OPEC+ has been aggressive with production cuts to keep prices high.

- The transition to green energy has slowed capital investment in new oil rigs.

- Conflict in the Middle East threatens the Strait of Hormuz.

In this environment, losing Russian barrels is not just an inconvenience; it is a systemic threat. The waiver extension acts as a pressure valve. It ensures that the plumbing of the global financial system doesn't clog up with "frozen" transactions that would lead to immediate delivery failures.

The Banking Dilemma

Financial institutions are notoriously risk-averse. Even with a waiver in place, many banks are "de-risking"—refusing to touch any transaction involving Russia because the compliance costs are too high and the reputational risks are too great. This creates a "chilling effect" that effectively tightens sanctions even more than the law requires.

By extending General License 8J, the U.S. government is trying to provide "comfort" to these banks. They are saying, "We promise we won't fine you billions of dollars for processing this specific type of payment." But even this is a temporary fix. It doesn't solve the long-term problem of how to handle a major global economy that has been partially disconnected from the world’s reserve currency.

Why China and India are Winning the Energy Game

While the U.S. and Europe grapple with the ethics of waivers and caps, India and China have become the primary beneficiaries of the current chaos. They are buying Russian crude at significant discounts—sometimes as much as $15 or $20 below the Brent benchmark. They then refine that crude into gasoline and diesel, much of which is eventually sold back to the West.

This is the great irony of the current sanctions regime. The oil is still reaching its destination; it’s just taking a longer, more expensive route that involves more middlemen. The U.S. knows this. They understand that if they were to truly "shut down" Russian oil, they would be forcing India and China to compete for the remaining supply from the Middle East, which would drive prices to astronomical levels for everyone.

The extension of the waiver is a nod to this global interdependence. It’s an acknowledgment that you cannot sanction a country that provides 10% of the world's energy without expecting to pay a price at home.

The Political Clock is Ticking

Policy decisions are rarely made in a vacuum, especially when an election is on the horizon. The current administration is acutely aware that high energy prices are a "silent killer" for incumbent governments. They can talk about unemployment rates and GDP growth all they want, but if the voter feels the pinch at the gas station or on their heating bill, the rest of the data doesn't matter.

This is why we see this recurring pattern of "tough talk" followed by "quiet extensions." The rhetoric is designed for the headlines; the waivers are designed for the economy.

The Cost of Consistency

If the U.S. were to be consistent, it would end all waivers and enforce the sanctions with total rigidity. This would certainly hurt Russia. It might even be the "tipping point" for their economy. But the cost would be a global recession.

- Manufacturing costs would spike as energy inputs become more expensive.

- Transportation costs for every physical good—from apples to iPhones—would rise.

- Central banks would be forced to keep interest rates higher for longer to fight the resulting inflation.

The "U-turn" isn't a mistake. It’s a survival tactic. It shows that despite the moral clarity often expressed in diplomatic speeches, the world of global finance and energy is governed by a much colder set of rules.

The Erosion of Financial Hegemony

There is a deeper, more permanent shift happening here. Every time the U.S. uses the dollar as a weapon and then has to walk it back with a waiver, the perceived power of those sanctions diminishes. Other nations are watching. They are seeing that the "almighty dollar" has limits.

Countries like Brazil, South Africa, and the Gulf states are increasingly looking for ways to settle trade in non-dollar currencies. They want to avoid being in a position where their own energy security is dependent on a license issued by the U.S. Treasury. This "fragmentation" of the global financial system is perhaps the most significant long-term consequence of the energy war.

By extending the waiver, Washington is trying to keep the current system alive for just a little bit longer. They are trying to manage a decline in influence while preventing a sudden, catastrophic break. It is a defensive play. It is the action of a superpower that has realized it cannot control the global market through decrees alone.

The extension of General License 8J proves that the energy transition is not happening fast enough to provide true strategic independence. As long as the world runs on hydrocarbons, those who control the taps—and those who control the payments for those taps—will be forced into uncomfortable compromises. We are seeing a superpower forced to choose between its foreign policy goals and its domestic stability. For now, the domestic wallet has won.

The illusion of a clean, decisive economic break from Russia has vanished, replaced by the gritty reality of a prolonged, messy stalemate where the lines between "sanctioned" and "essential" are increasingly blurred.

The next time a politician promises to "bankrupt" an adversary through sanctions, look for the fine print in the Treasury Department's next waiver extension. It is there that the real policy is written.

The global energy market is too large to be bent to the will of any single capital, and as long as the world’s thirst for oil remains unquenched, the pragmatic "U-turn" will remain the most powerful tool in Washington’s arsenal.