The financial press is obsessed with the Fed's "looming battle." They treat the balance sheet like a ticking time bomb, a monstrous pile of debt that will eventually crush the global economy under the weight of Quantitative Tightening (QT). They are wrong. They are chasing a ghost.

The real danger isn't the size of the Fed’s assets. It’s the terminal misunderstanding of what those assets actually do. Most analysts talk about the $7 trillion-plus balance sheet as if it’s a pile of cash sitting in a vault that needs to be "paid back." It’s not. It’s a plumbing fixture. And right now, the plumbers are arguing about the color of the pipes while the basement is flooding.

The Myth of the Neutral Balance Sheet

The biggest "lazy consensus" in macroeconomics today is the idea of a "neutral" balance sheet—some magical pre-2008 level that we must return to for the sake of "normalcy." This is nostalgia masquerading as analysis.

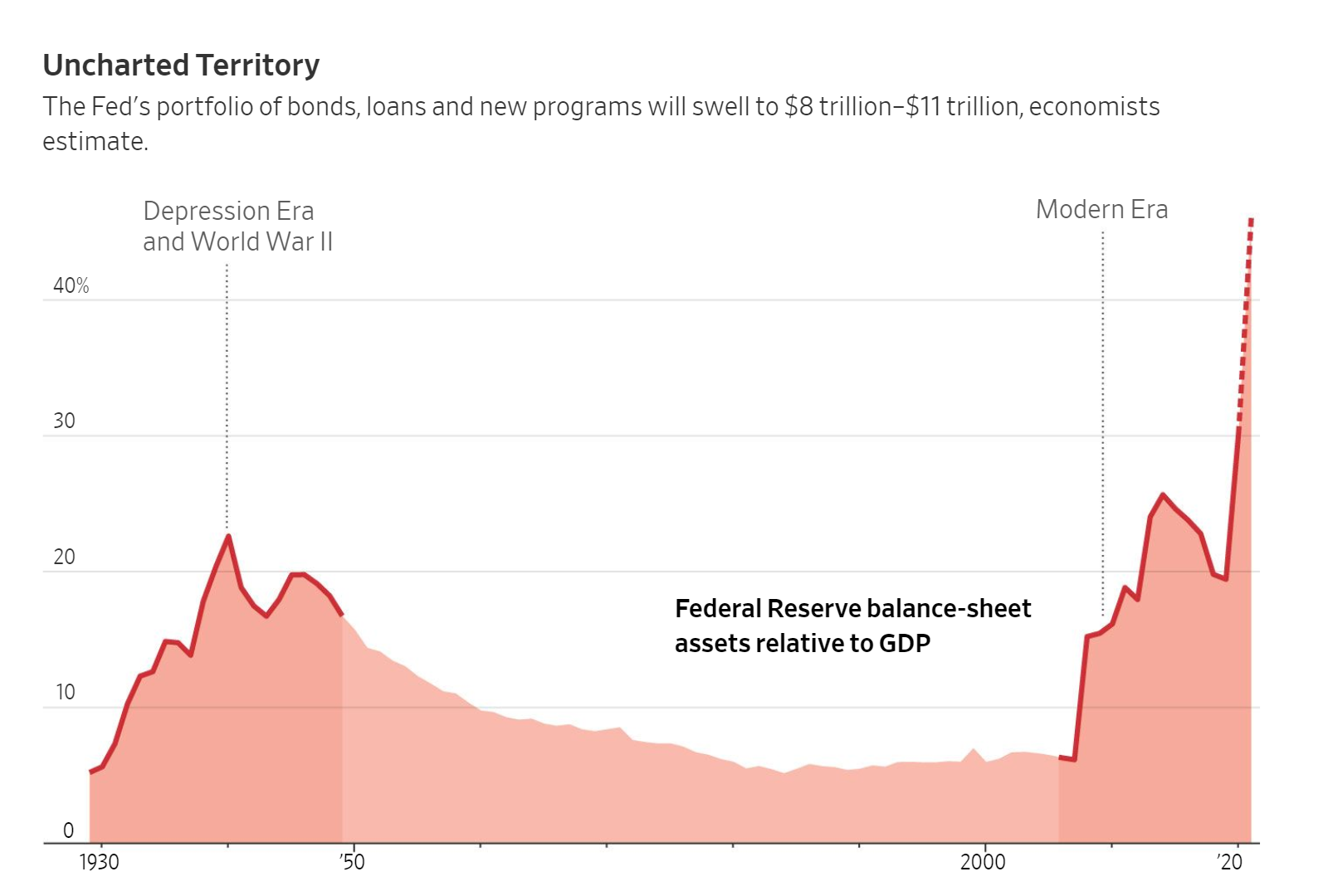

We are never going back to the $800 billion footprint of the early 2000s. The financial system has fundamentally changed. Regulatory requirements like the Liquidity Coverage Ratio (LCR) mean that banks now have a structural, permanent thirst for central bank reserves. If the Fed shrinks the balance sheet too far in an attempt to "return to normal," they don’t achieve stability. They trigger a liquidity seizure.

I’ve watched traders lose their shirts betting on a "return to mean" that never comes because they ignore the regulatory floor. The Fed isn't holding these assets because it wants to; it’s holding them because the private banking system is now legally required to be addicted to them.

Quantitative Tightening is a Psychological Magic Trick

The "battle" over QT is largely theater. The consensus view is that QT drains liquidity and acts as a massive drag on equities. In reality, the correlation is messy at best and coincidental at worst.

When the Fed rolls off Treasuries, it doesn't just disappear money from the universe. It shifts the duration risk back to the private sector. The "drain" only matters if the private sector lacks the appetite to hold that duration. Currently, the world is starving for high-quality collateral.

Stop asking, "When will the Fed stop QT?"

Start asking, "When will the Treasury stop over-supplying the front end?"

The Fed’s balance sheet is the tail. The Treasury’s issuance schedule is the dog. If you’re watching the tail to see where the dog is running, you’re going to get bitten.

Why the Repo Market is the Only Real Signal

People also ask: "Will the Fed’s balance sheet cause a crash?"

The answer is no, but the plumbing of the balance sheet might. Look at September 2019. The Fed was shrinking its holdings, everything looked fine on paper, and then the repo market—the heartbeat of Wall Street—suddenly spiked to 10%. Why? Because the Fed hit the "lowest comfortable level of reserves" (LCLoR) without realizing it.

The "battle" isn't about the total dollar amount. It's about the distribution. You can have $10 trillion in reserves, but if they are all parked at JPMorgan and Citigroup while the smaller players are starving for cash, the system breaks.

The Fed’s current dilemma isn’t "too much money." It’s "immobile money." The Standing Repo Facility (SRF) was created to fix this, acting as a pressure valve. If you aren't monitoring the usage of the SRF and the Reverse Repo Facility (RRP), you aren't actually tracking the Fed’s impact. You’re just looking at a big number and feeling scared.

The Inflation Fallacy

The most tired argument in the room is that a large balance sheet is inherently inflationary.

If that were true, the decade between 2008 and 2018 would have seen hyperinflation. Instead, we struggled to even hit 2%. The balance sheet only becomes inflationary when it facilitates direct fiscal transfers—when the government hands out checks and the Fed prints the offset.

When the Fed holds bonds on its balance sheet, it is performing a maturity swap. It takes a long-term bond out of the market and replaces it with a short-term reserve. This is a volatility dampener, not a kerosene soak for consumer prices. The inflation of 2021-2023 was a supply chain and fiscal stimulus story, yet the "hard money" crowd still wants to blame the Fed’s balance sheet for the price of eggs. It’s intellectually dishonest.

The Brutal Reality of Net Interest Income

Here is the part the Fed doesn't want to talk about, and the "experts" ignore because it’s messy: The Fed is currently losing money.

By raising rates while holding a mountain of low-yield bonds, the Fed is paying out more in interest to banks (on their reserves) than it is earning on its own portfolio. This creates a "deferred asset" on their books. In plain English: it’s a loss.

Does it matter for the Fed’s ability to function? No. They can't go bankrupt.

Does it matter for politics? Absolutely.

The "battle" isn't over economic theory; it’s over the optics of the central bank sending zero dollars to the Treasury for years while paying billions to commercial banks. This is the friction point that will actually force the Fed’s hand. They will stop QT not because the economy needs it, but because the political heat of their "loss" becomes unbearable.

Stop Trying to "Normalize" the Balance Sheet

The obsession with a smaller balance sheet is a remnant of a gold-standard mindset in a digital-reserve world.

A large balance sheet is a tool for financial stability in a world of massive, instantaneous capital flows. Shrinking it to satisfy a sense of "moral rectitude" is like a pilot turning off the engines mid-flight because he thinks using too much fuel is "improper."

The real risk is a "Taper Tantrum 2.0," not because of the size of the roll-off, but because of the communication gap. The Fed is trying to be transparent, but the market interprets transparency as a promise. When the Fed inevitably has to pivot and start growing the balance sheet again to provide liquidity, the consensus will scream "Pivot! Pivot! Inflation is coming!"

They will be wrong again. Growing the balance sheet during a liquidity crunch isn't stimulus; it's maintenance.

The Counter-Intuitive Play

If you want to survive the next five years of "Fed battles," ignore the top-line asset number.

- Watch the RRP drain. When the Reverse Repo Facility hits zero, that’s when the real QT begins. Everything before that was just "excess" liquidity leaving the room.

- Ignore the "money printing" memes. Reserves are not M2 money supply. They are different animals.

- Bet on the "Floor System." The Fed has moved to an "ample reserves" framework. This means the balance sheet will always be larger than you think it should be. Stop betting on a "crash" caused by its size.

The Fed isn't fighting a battle over its balance sheet. It’s managing a permanent expansion of its role as the world’s backstop. The "looming battle" is a headline for people who still think it’s 1995.

The balance sheet isn't the problem. The belief that it needs to be small is.

Sell the fear. Buy the liquidity floor.